Massive corporate tax crackdown

Cook AP

Author

Partially in response to the PwC scandal, and also delivering on an election promise, the Albanese Government has introduced sweeping changes to tax enforcement, delivering record corporate tax receipts and the biggest crackdown on adviser misconduct in Australian history.

Australia's tax system faced a significant credibility challenge in 2023 when the PwC tax leaks scandal exposed severe shortcomings in how tax advisers and large corporations were regulated. The scandal revealed how confidential government information could be misused to help clients avoid tax, highlighting weaknesses in Australia's regulatory frameworks that had persisted for decades.

In response, the Albanese Government launched a three-pronged reform agenda: strengthening tax system integrity, increasing regulator powers, and overhauling regulatory arrangements.

At the core of these reforms is a recognition that tax avoidance schemes have evolved to become more sophisticated and complex, often operating across jurisdictional boundaries, while the laws governing them remained static. The previous promoter penalty laws, designed primarily for mass-marketed schemes of the 1990s, had only been used six times since their creation.

Key Changes Include:

For Tax System Integrity:

Broadened definition of 'promoter' to capture those receiving benefits from scheme promotion

Extended timeframes for civil penalty proceedings from 4 to 6 years

Dramatically increased maximum penalties

For Regulatory Powers:

New powers for regulators to share information about misconduct

Protection for whistleblowers reporting to the Tax Practitioners Board

Extended investigation timeframes from 6 to 24 months

Enhanced public register of tax practitioners

New ability to refer misconduct to professional associations

For Regulatory Framework:

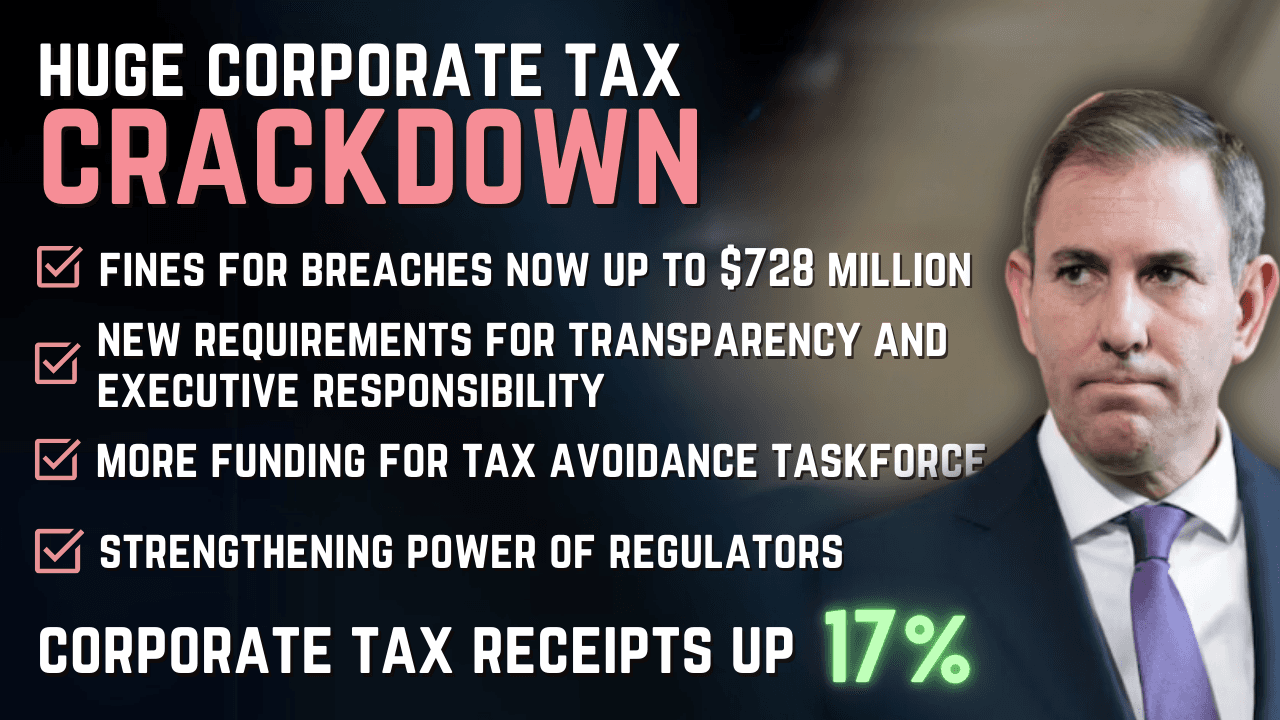

New requirements for transparency and executive responsibility

Enhanced management of conflicts of interest

Strengthened governance obligations for large firms

The penalties have been particularly strengthened. For significant global entities (those with annual global income over $1 billion), maximum penalties can now reach $782.5 million - calculated as the greater of:

$15.7 million

Three times the benefit received

10% of aggregated turnover (up to $782.5 million)

These reforms appear to be having an impact. Corporate tax receipts reached almost $100 billion in 2022-23, representing a 17 percent increase from the previous year. This follows increased investment in the ATO's compliance operations, including around $200 million per year in additional funding for the Tax Avoidance Taskforce.

The Government states these increased receipts directly support essential services including healthcare, infrastructure, and education, while positioning Australia as a world leader in corporate tax compliance.

[1] https://ministers.treasury.gov.au/ministers/jim-chalmers-2022/media-releases/government-taking-decisive-action-response-pwc-tax-leaks

[2] https://www.ato.gov.au/media-centre/ato-collects-100-billion-dollars-from-large-corporates

[3] https://treasury.gov.au/sites/default/files/2023-09/factsheet-government-response-pwc-tax-leaks-scandal_0.pdf